Proxy revenue swaps for solar

Risk-transfer products, such as volume puts or swaps, are now standard product offerings, serving as offtake arrangements in lieu of traditional power purchase agreements.

One of these products, the proxy revenue swap, debuted in 2016 and caters specifically to the needs of wind energy projects.

In response to industry demand, the scope has now been extended to include solar energy. The first set of proxy revenue swaps for two solar projects in Queensland, Australia was executed in May 2018, covering a total installed capacity of 176 megawatts. Unlike virtual power purchase agreements or fixed-volume swaps, proxy revenue swaps hedge shape risk in addition to price and volume risk.

Understanding shape risk

As markets and technology are maturing, many projects are now run as merchant plants and are, therefore, exposed to both volume and price risk.

There is an additional risk that is less obvious: shape risk, which involves the relationship between volume and price.

Solar energy is non-dispatchable and weather driven. When the sun shines, solar farms will come online, and will all produce at the same time. This clustering of production depresses the market clearing price. Consequently, to determine the revenue that a solar project will earn, it is no longer enough to know the total volume produced and the average market price; when the power is produced is as important.

In many markets, the midday hours used to have the highest energy prices. This is no longer the case. The quantity of solar energy produced is usually at a peak at midday, and the combined volume of all solar generation can result in very low and even negative prices, as has happened in several jurisdictions.

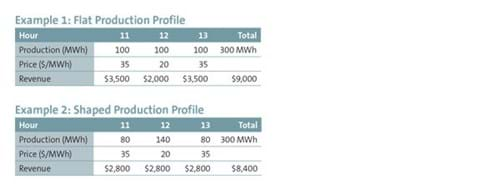

As a simple example, assume that a solar farm has a total production of 300 megawatt hours over the three hours around noon and that the average spot price over that period is $30 a MWh. Here are two examples of the potential shape of that production:

In both cases, the total energy and the average price are the same. However, the revenue is significantly lower in the second case, as the highest volume is produced in the lowest priced hour. In the first example, the production-weighted price is $9,000 divided by 300 MWh = $30/MWh, whereas in the second case the production-weighted price is $8,400 divided by 300 MWh = $28/MWh.

The point is that shape risk affects total revenue in a market with fluctuating prices.

Counterintuitively, the risk is greater when all solar production within a market is highly correlated.

When one solar facility starts producing during a sunny hour, so will every other solar farm in the same market. As supply increases, the market-clearing price decreases. This can lead to situations with many hours where a project produces more energy, but earns less total revenue.

When the market penetration of renewables was still low, the revenue risks associated with the shape of production were negligible. However, as market penetration of renewables is increasing, the shape risk will increase drastically.

Proxy revenue swap

To address the issue of protecting revenue streams for renewable assets, Nephila Climate, in conjunction with Allianz Risk Transfer and REsurety, pioneered an innovative risk-transfer product called a proxy revenue swap. This form of swap was designed originally to meet the needs of the wind energy industry, but it has now been adapted also to cover solar facilities and has the potential to make more solar projects bankable by de-risking project revenues.

Several projects using proxy revenue swaps as an offtake have been successfully financed by major lenders (such as Deutsche Bank) and tax equity players (such as JP Morgan and Goldman Sachs). The product has been used in US markets like ERCOT and SPP, and now also in the Australian AEMO market.

Under a solar proxy revenue swap, the hedge provider pays the project a fixed lump-sum amount per quarter, regardless of the level of irradiance, (intensity of sunlight), the volume and timing of the energy produced by the project, and the market-clearing price for electricity. The project pays the hedge provider a floating amount each quarter equal to the “proxy revenue.” The “proxy revenue” for a quarter is the sum of the “proxy revenue” for each settlement period in the relevant electricity market for that quarter. (For example, the settlement period for the Australian AEMO market is 30 minutes.). The proxy revenue for a given settlement period is calculated as the hub price multiplied by the project’s “proxy generation” for the settlement period. The proxy generation for each settlement period is determined using a pre-agreed formula that converts irradiance, or the strength of local sunlight, into an amount of electricity output.

Because the fixed payment is not linked to actual output, the solar proxy revenue swap offers a predictable revenue stream and mitigates irradiance risk, price risk and shape risk for the project.

As fixed operational efficiencies are assumed in the calculation of “proxy generation,” the operating risks, such as availability of the project, stay with the project.

The proxy revenue swap is a financial hedge, meaning no energy is purchased as part of the transaction. Instead, the energy produced by the project is sold into the local grid, with the project collecting revenues at the nodal price for that electricity.

Separately, the hedge is settled quarterly with the hedge provider paying the fixed amount and the project paying the floating “proxy revenue.” If the fixed amount exceeds the “proxy revenue” amount for a given quarter, then the hedge provider makes a payment to the project equal to the difference. If, on the other hand, the “proxy revenue” exceeds the fixed amount, then the project makes a payment to the hedge provider equal to the difference. Ostensibly project payments are sourced from merchant revenues.

The proxy revenue is calculated using the electricity price at a market hub determined by the parties. A “hub” is used because there is more electricity trading and liquidity than at the node, thus allowing the hedge provider greater flexibility in managing its exposure. The risk that the revenue the project actually receives (based on the nodal price) differs from the price at the hub is called “basis” risk. It remains with the project.

Although the energy produced is not actually sold to the hedge provider under the proxy revenue swap, sometimes the hedge provider will purchase the associated environmental attributes.

Given that the availability is one of the assumptions in the calculation of “proxy generation,” the proxy revenue swap does not contain any availability requirements. Furthermore, the hedge does not contain minimum delivery obligations. Credit-support obligations are similar to those in other types of energy hedges; for example, the project might be required to provide a letter of credit or cash collateral as credit support to ensure the project has the means to make payments required under the hedge.