July 9, 2015 | By Keith Martin in Washington, DC

Xuanwu Jin, with the Sunshine Law Firm in Hangzhou

China is moving to form a New Silk Road Fund and an Asian Infrastructure Investment Bank that will finance power and other infrastructure projects along six corridors in Asia, the Middle East and eastern and northern Africa.

They are both part of a “One Belt, One Road” development strategy that China hopes will lead to greater cooperation among countries on Asian, European and African continents.

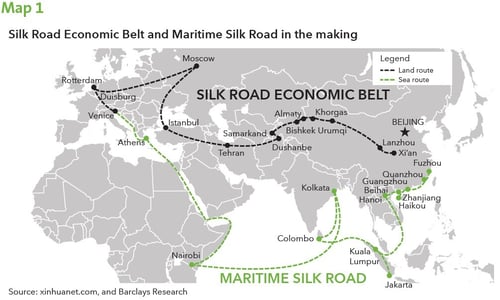

The strategy has two main components — a land based “Silk Road Economic Belt” and the oceangoing “21st Century Maritime Silk Road.” Both were first unveiled by Chinese President Xi Jinping during visits to Kazakhstan and Indonesia in 2013, but have since attracted close attention.

The Silk Road Economic Belt is an initiative to improve land transportation such as road and rail routes and other means of connection, including oil and natural gas pipelines and IT infrastructure, in an area that stretches from China to central and South Asia, Russia, the Mideast and Europe. As its equivalent on the sea, the 21st Century Maritime Silk Road is an initiative to create a network of ports and industrial parks scattered across South and Southeast Asia, East Africa and the northern Mediterranean Sea.

In addition to infrastructure development and construction, the One Belt, One Road development strategy also calls for promoting greater financial integration and removing trade barriers such as customs and restrictive border controls in the regions. There will be a particular emphasis on strengthening cooperation in the energy sector through investing in new projects and establishing investment zones.

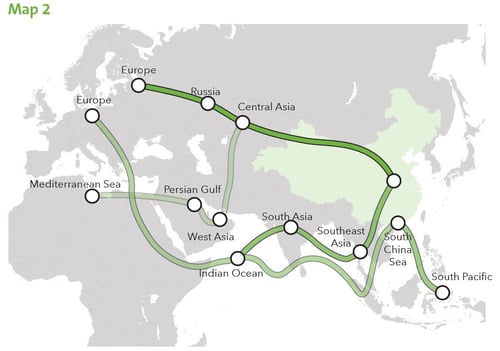

China is considering developing up to six major economic corridors along the Belt and Road, according to a recent blueprint released by China’s top economic planning agency, the National Development and Reform Commission (NDRC). The six corridors are shown in map 2 and are referred to in China as the New Eurasian Land Bridge, China-Mongolia-Russia, China-Central and Asia, China-Indo-China Peninsula, China-Pakistan, and Bangladesh-China-India-Myanmar.

A number of new financial institutions have been established to provide financial support. The most important are the New Silk Road Fund (NSRF) and the Asian Infrastructure Investment Bank (AIIB), which are considered to be the financial arms of the “One Belt, One Road” strategy.

The NSRF was established in late 2014 in the form of a limited liability company under Chinese law with an initial capital of US$40 billion. It will fund investment that is essential to the development of trade routes along the “One Belt, One Road” area. The initial shareholders of the fund are all from China, including the country’s sovereign fund, China Investment Corp., and two leading Chinese policy banks — The Export-Import Bank of China and China Development Bank. However, the fund will be open to investors from other countries. The fund has already started operation. A memorandum of understanding for a pilot hydroelectric project in Pakistan was signed on April 20, 2015.

AIIB

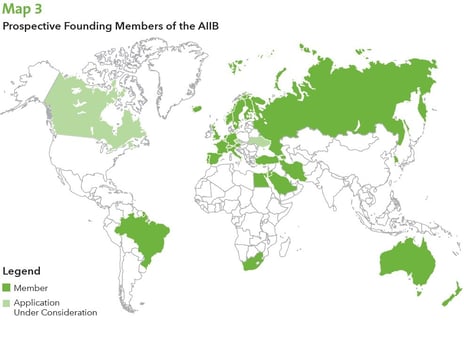

The AIIB was designed to be a multilateral organization and to mimic the roles of several Washington-based international lending institutions and the Asian Development Bank in Manila. It has currently 57 founding members comprised of 37 Asian countries, 18 European countries, Australia, New Zealand, two African countries and Brazil. The authorized capital of the AIIB is expected to be US$100 billion and will be used exclusively for infrastructure projects in sectors such as energy, transportation, telecommunications, agricultural development, urban development and logistics in Asia.

As a regional development bank, AIIB’s regional members will be the majority shareholders while non-regional members will hold smaller equity shares of the bank. Seventy-five percent of the AIIB shares will be reserved for Asian countries, of which China and India are supposed to hold 25% and 10% respectively. This shareholding arrangement reflects the commitment and ownership of regional members while providing non-regional members the opportunity to participate. The prospective founding members of the AIIB are shown in map 3.

The AIIB will make loans and equity investments and provide guarantees. In addition to the capital subscribed by members, it is anticipated that the AIIB will raise funds primarily through the issuance of bonds in world financial markets as well as through the inter-bank market transactions and other financial instruments.

The founding members agreed on the articles of association of the bank in May 2015. Upon signing, signatories to articles will start their domestic ratification procedures. The AIIB is expected to start operations by the end of 2015. It is supposed to fill a gap between the region’s infrastructure financing needs and the financial resources available from existing multilateral and bilateral development institutions.

Additional funding for such projects may soon be available. Another new development bank is being established by the BRICS — Brazil, Russia, India, China and South Africa — that will have a capital of US$100 billion and a reserve currency pool worth another US$100+ billion. A separate new Shanghai Cooperation Organization development bank is being established by Russia and China to focus on financing interstate infrastructural projects and foreign trade cooperation.

China is trying to address two problems with one leap with the “One Belt, One Road” strategy.

China’s economic growth is slowing down. The days when it enjoyed double-digit growth rates are gone. The growth rate for 2014 was 7.4% and is expected to slide to 7% in 2015. To make things worse, overcapacity that was caused by the US$4 trillion economic stimulus package introduced to combat the financial crisis of 2008 is taking its toll on the country’s economy. The industry sectors that received massive financial aid through the stimulus are now all struggling with overcapacity. The most affected sectors are steel, cement, aluminum and photovoltaics, each having an average capacity utilization around only 70%. Therefore, exploring new markets overseas has become vital for the Chinese economy.

At the same time, Asia faces a massive infrastructure gap. Many Asian countries have long been suffering from outdated or insufficient infrastructure devolvement. The Asian Development Bank (ADB) estimates that for the period between 2010 to 2020, Asia needs US$8 trillion for infrastructure construction. Unlike countries such as China and Japan, the majority of Asian countries have neither the money nor the industrial capability to undertake infrastructure overhauls that are considered long overdue. The ADB is doing the best it can to help with the situation, but a little help from a new lender should be welcome: apart from infrastructure projects, the ADB invests in a wide range of projects such as public health and education, which means only a fraction of its US$160 billion capital is devoted to infrastructure; in contrast, the newly-established AIIB will apply all of its US$100 billion exclusively to infrastructure.

Chinese Outbound Investment

China has also made recent regulatory changes to promote outbound investment. China launched a “going out” strategy 10 years ago to encourage Chinese companies to make overseas investments and acquisitions. Chinese companies are expected to gear up their outbound investment activities further in view of the additional financial support on offer. In the meantime, the latest, and by far the most significant, round of legal reforms has been completed, setting the stage for a new wave of outbound investment. Three Chinese regulatory bodies — the National Development and Reform Commission (NDRC), the Ministry of Commerce (MOFCOM) and the State Administration of Foreign Exchange (SAFE) — each rolled out new rules loosening state control of outbound investment in the last year (see table 1). The new regime supersedes a previous one that had been in place since 2004.

No more registration with SAFE, banks keep records of foreign exchange use, no extra procedure to be followed.

The new regime shifts from an approval-based process to a filing-based process, reduces the number of outbound investments that needs approval of the government and shortens the time required for approval. It also cancels the requirement of foreign exchange registration with SAFE to allow funds to move more quickly. The administrative procedures for overseas investment have been significantly simplified.

The business sector has reacted positively to the changes. Outbound investment in foreign companies by Chinese firms soared to a record high of 246 in 2014, an increase of 30% compared to the year before. The trend continues in 2015: in the first quarter of 2015, 77 deals were completed with an aggregate deal value of US$20.2 billion. Both figures are record highs. Although popular investment destinations include all countries along the Belt and Road, ASEAN stands out as a key region largely because it is currently hosting most of the member states of the AIIB.

Eighteen European countries have following the lead of the United Kingdom and joined the AIIB as founding members. Being founding members gives these countries the right to participate in formulating the new bank’s policies. This is important in view of concerns about transparency of how the AIIB will be governed. There are, of course, more tangible benefits. Joining the AIIB will allow these countries to tap into the huge infrastructure market in Asia. Countries like the UK, Germany and France all have companies with household names in the infrastructure sector in the region. These companies are expecting to reap the economic benefits by landing contracts relating to projects that are financed by the AIIB. Smaller companies from other European countries will be trying to land sub-contracts with the bigger firms.

Another opportunity from which the European countries may benefit is the new bank may decide to raise capital by issuing bonds, given that the AIIB’s initial capital of US$100 billion is still modest compared to the ADB’s capital of US$165 billion, let alone the US$8 trillion funding shortage for infrastructure in the region. Any such bonds may be placed in European markets.![]()