Renewable Energy Opportunities in The Middle East

Jordan has initiated the second round of its unsolicited proposals scheme that permits developers to submit renewable energy project proposals directly to the government.

The Kingdom’s Ministry of Energy and Mineral Resources, or MEMR, is seeking expressions of interest from qualified investors interested in developing renewable energy projects on a build, own and operate basis. The deadline to submit an electronic and hard copy response is October 31, 2013.

The first round of unsolicited proposals extended to an array of renewable energy sources such as wind, solar, waste and geothermal, but this round is restricted to wind and solar.

MEMR launched the first round of unsolicited proposals in May 2011. Thirty-four applications including 12 wind projects, 15 solar photovoltaic projects, two concentrating solar photovoltaic projects and five solar thermal projects initially qualified. However, only two wind projects and 12 solar photovoltaic projects were eventually approved. The aggregate capacity of the two wind projects is approximately 200 megawatts, and the aggregate capacity of the 12 solar photovoltaic projects is also around 200 megawatts. In May 2013, MEMR received proposals for each of the approved projects. Formal project awards are still pending, and MEMR is currently hosting clarification meetings with a number of bidders.

The launch of the second round prior to the completion of the first round has surprised the market, although this is consistent with Jordan’s aim to reduce its dependence on imported energy — 97% of the energy it used in 2011 was imported — and increase the share of renewable energy contributions from 1% in 2011 to 10% by 2020.

The near finalization of the first round combined with the launch of the second round positions Jordan as the Middle East’s most active and arguably advanced renewable energy market.

International renewable energy developers should view Jordan as a place to plant a flag in the Middle East and eventually as a stepping stone toward other high potential, but currently less active, regional markets, including Saudi Arabia with its colossal program to procure 54,000 megawatts of renewable energy facilities by 2032.

Amidst the high hopes and hype surrounding the Middle East’s apparent drive towards renewable energy, and solar power particularly, the reality is that the pace of deploying commercial procurements has been sluggish. Very few renewable energy tenders have recently come to market.

At present, the key Middle Eastern renewable energy markets are Jordan, Saudi Arabia, the United Arab Emirates, Kuwait and, with some reserve, Qatar.

Jordan: Notable Points

An applicant’s expression of interest to MEMR must include a description of both the applicant and the project, evidence of the applicant’s technical capability and experience and a demonstration of the applicant’s ability to raise debt and equity.

The applicant must provide a project description, including the location with coordinates on a map, capacity and estimated generation per year and envisaged wind or solar power technology.

In the first round, MEMR chose to focus most of its efforts on the southern region of Ma’an and, in particular, an 8.75 square kilometer zone dubbed the Ma’an Development Area, or MDA. The MDA is attractive because the applicable regulatory and administrative regime is more streamlined and flexible than would otherwise be in Jordan; the fiscal regime is also more advantageous. The MDA is also attractive from a resource standpoint. The area had been earmarked as the best location in Jordan for concentrated solar power projects by Lahmeyer International, a Germany-based technical advisor. MEMR’s initial focus in the first round was on concentrated solar power.

In the second round, Jordan wants to shift the focus away from the Ma’an region towards the northern and eastern parts of Jordan. MEMR said explicitly in its expression of interest request that submissions for projects in those parts of the country will be prioritized. The key driver behind this geographic shift is to ease the pressure on the already fragile grid in the southern part of the country. The grid in the northern and eastern parts of Jordan is currently less saturated.

The northern and eastern parts of Jordan may pose a number of challenges to wind and solar developers. First, there is no MDA equivalent; although, there are rumors that the granting of development area status for a specific parcel of land is being considered. Second, the northern and eastern parts of Jordan are more industrialized than the Ma’an region, which could lead to complications, particularly in terms of land rights and permits. Third, proximity to the border with war-torn Syria cannot be ignored; certain plots being targeted by developers are only around 25 kilometers from the Syrian border, and even closer to the growing refugee camps inside Jordan.

In its expression of interest request, MEMR said the applicant must contact the relevant transmission or distribution company to establish the suitability of the envisaged grid connection at the proposed location.

On the basis of round one precedent, interested parties are not expected to furnish documentation to substantiate any exchange with the transmission or distribution company. A mere mention in the expression of interest that exchanges between the developer and the transmission or distribution company have taken place and identifying the proposed location for the envisaged grid connection should suffice.

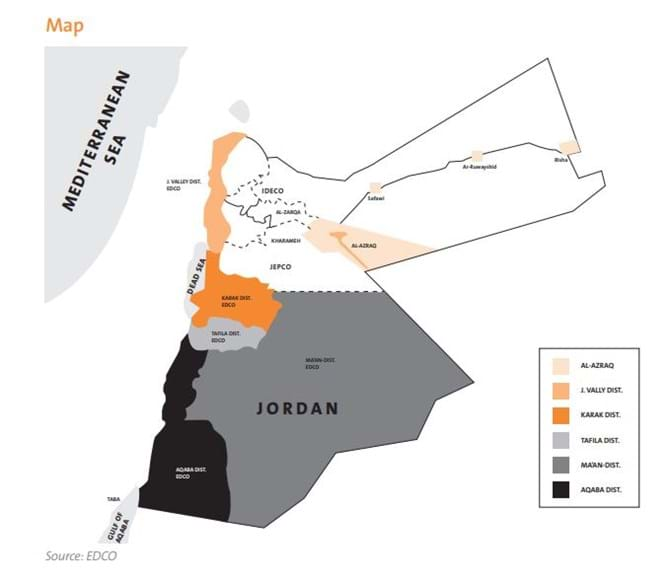

If the developer connects at a high voltage level, the interconnecting utility, and ultimately the power purchase agreement counterparty, will be Jordan’s sole transmission company, NEPCO. Otherwise, the counterparty will be one of Jordan’s three distribution companies: Jordanian Electric Power Company, or JEPCO, Electricity Distribution Company, or EDCO, and Irbid District Electricity Company, or IDECO. As illustrated in the map below, each of the distribution companies could be relevant in round two. JEPCO operates in the north, EDCO in the northwest and in the east, and IDECO operates both in the northern and eastern parts of the country.

The power purchase counterparty will be an important consideration. First, there is an asymmetry of interest for each of the transmission company and the distribution companies to adopt renewable energy-based power. Second, varying experience levels mean that power purchase agreement negotiations may be more laborious with certain parties. NEPCO, for instance, has procured and successfully banked four major conventional independent power projects in the Kingdom: the 370-megawatt Amman East IPP (the first independent power project in Jordan), the 373-megawatt Al Qatrana IPP, the 573-megawatt IPP 3 and the 241-megawatt IPP 4.

Applicants that submit an expression of interest and qualify to bid will receive a memorandum of understanding from MEMR enabling each to proceed with measurement campaigns, feasibility studies and other preparatory and due diligence work such as negotiating land access and financing options. The form of memorandum of understanding in round two is likely to be substantially the same form as in round one.

Once the steps outlined in the memorandum of understanding are completed, the applicant is required to submit a full and committed proposal in compliance with the provisions of the applicable laws and regulations. All proposals must be submitted within the time period specified in the memorandum of understanding.

The Renewable Energy and Energy Efficiency Law requires any unsolicited proposal to generate electricity and connect to the grid must meet four conditions.

First, the proposal must contain a development plan including the preliminary design, initial financing plan, and the contribution of local inputs to the facility, supplies, construction and operation. Second, the bidder must demonstrate that it has experience with similar renewable energy facilities. Third, the bidder must include any documents or additional data necessary to fully appraise the proposal. Finally, the proposed electricity tariff must be a fixed tariff expressed as an amount per kilowatt hour and be within an acceptable range according to Jordan’s so-called reference price list.

Electricity Prices

The reference price list prescribes the pricing mechanism for the purchase of electrical power from renewable energy sources. It is issued by Jordan’s Electricity Regulatory Commission, or ERC.

The reference price list sets a separate electricity tariff cap for electricity generated by wind facilities, solar photovoltaic facilities, non-photovoltaic solar power facilities, biomass facilities and biogas facilities. The tariff cap for electricity generated by a wind power facility is JD 0.085/kWh (approximately US$0.12/kWh). For a solar photovoltaic facility, the tariff cap is JD 0.12/kWh (approximately US$0.17/kWh), whereas the tariff cap for a non-photovoltaic solar power facility is JD 0.19/kWh (approximately US$0.183/kWh).

The reference price list also includes a localization incentive. If a winning bidder installs a renewable energy facility that is of “fully Jordanian origin,” then the proposed tariff will be increased by 15%. The ERC’s council of commissioners may terminate the localization incentive once 500 megawatts of renewable energy facilities are connected to the grid.

The council of ministers is permitted to review the reference price list on an annual basis or whenever deemed necessary.

MEMR or any other entrusted body has six months from bid submission to notify the bidder of its decision. If initial approval is granted, then the energy minister is required to submit its recommendations to the council of ministers for it to issue a final decision.

Out of the 34 shortlisted projects in round one, only two wind projects and 12 solar photovoltaic projects were eventually approved.

In May 2013, MEMR received proposals for each of the approved projects. Since early September 2013, MEMR has been hosting clarification meetings with bidders. This is because a number of bidders proposed a tariff that deviates from the feed-in tariff and a capacity that differs from what had initially been approved.

The submission of these “alternative” proposals has caused a stir in the market. MEMR has reportedly asked the council of ministers to resolve whether it may negotiate the proposed tariff and capacity with bidders, or whether the feed-in tariff should be honored.

Despite some of the challenges experienced in the first round, round two will undoubtedly generate considerable market interest, and probably more than in the first round.

First, the drivers for Jordan to adopt wind and solar power remain very strong. Of the energy Jordan used in 2011, 97% was imported. Such acute dependence on imports also has major security implications, especially in the context of ongoing regional instabilities.

Second, the barriers to entry in the Jordanian renewable energy market are relatively low. For instance, bidders will not be required to provide a bid bond.

Saudi Arabia

Saudi Arabia is the market with the highest potential and, accordingly, the key focus of most market participants.

By 2032, the Kingdom plans to issue procurements for 25,000 megawatts of solar thermal projects and 16,000 megawatts of solar photovoltaic projects worth more than US$60 billion, plus another 13,000 megawatts of wind, geothermal and waste-to-energy plants.

The first step in the process was the release of a white paper in late February 2013 by the King Abdullah City for Atomic and Renewable Energy or K.A.CARE, Saudi Arabia’s renewable energy procurement agency.

One month after the white paper was issued, K.A.CARE was due to issue both a draft request for proposals and a draft power purchase agreement marking the onset of an introductory procurement round of up to 800 megawatts of renewable energy facilities, including approximately 600 megawatts of solar and 100 megawatts of wind. To date, no such documents have been issued, which means that the program is already half a year behind schedule.

The rollout of the program depends on K.A.CARE’s financial empowerment. This, in turn, requires the approval of an implementing regulation by the Saudi Arabian Council of Ministers.

Arguably, the deployment of the program also hinges on garnering sufficient buy-in from Saudi Aramco. Sources say that Saudi Aramco’s increasingly apparent lack of buy-in on the K.A.CARE program has caused friction and may continue to do so. A few months ago, market rumours went as far as suggesting that Saudi Aramco may take control of the program.

The need for an implementing regulation together with the need to co-opt key stakeholders such as Saudi Aramco means that the timing for the launch of K.A.CARE program procurements is uncertain and that further delays are to be expected. It is unlikely that tenders will be issued in 2013.

There are opportunities beyond K.A.CARE’s program, however. Saudi Electricity Company, the state-controlled listed electric utility, is set to launch tenders for two gas-fired integrated solar combined cycle projects in Dibba City.

In 2013, Saudi Electricity Company plans to tender the Dibba 1 IPP, a 550-megawatt integrated solar combined-cycle project. The solar power component reportedly amounts to 30 megawatts. Saudi Electricity Company expects the project to be completed in 2016. Tender issuance is dependent on Saudi Electricity Company securing land which is reportedly underway.

In 2014, Saudi Electricity Company plans to tender the Dibba 2 IPP, a 1,800-megawatt integrated solar combined-cycle project. The solar portion has yet to be confirmed.

Saudi Electricity Company expects this project to be completed in 2017.

For each of Dibba 1 IPP and Dibba 2 IPP, the procurement will be undertaken on a build-own-and-operate model. The solar power technology, in each case, has yet to be confirmed.

Saudi Electricity Company is the key procuring entity for conventional power in Saudi Arabia and has developed a well-oiled independent power project procurement model. In recent years, it banked the 1,200-megawatt Rabigh 1 independent power project, the 1,729-megawatt Riyadh PP11 independent power project and the gargantuan 3,927-megawatt Qurayyah independent power project, currently the largest independent power project in the world.

United Arab Emirates

The two key markets in the United Arab Emirates are the Emirates of Abu Dhabi and Dubai. Each emirate has its own utility — the Abu Dhabi Water and Electricity Authority and the Dubai Water and Electricity Authority — and each develops and issues its own independent policies and procurements, subject to federal laws.

Abu Dhabi plans to generate 7% of its electricity from renewable sources by 2020 while Dubai has a 5% target. The key focus in the United Arab Emirates is solar power.

Abu Dhabi has been at the forefront of renewable energy developments. Last year, it commissioned the Shams 1 solar power project, a 100-megawatt solar thermal project. The project was precedent setting for a number of reasons, but the key reason is that it was the first utility-scale solar power facility in the Gulf to be procured on an independent power project basis.

Shams 1 was developed largely on the basis of the Abu Dhabi Water and Electricity Authority independent power project model for conventional power. This model has been banked on numerous occasions and is arguably one of the Middle East’s most advanced independent power (and water) project models.

Masdar, a wholly-owned subsidiary of the Abu Dhabi government-owned Mubadala Development Company, is procuring the 100-megawatt photovoltaic Noor-1 project, which was intended to figure as the first phase of a 200-megawatt solar park. The preferred bidder has yet to be to be selected, however, and severe delays have caused uncertainty as to whether the project will ever follow through.

Although in a regional context Abu Dhabi’s track record is impressive, from a forward-looking perspective, opportunities for renewable energy developers, at least in the short-to-medium term, are somewhat limited. The only concrete and notable development is the possible launch of a solar photovoltaic rooftop program. This plan has been in the pipeline for several years, however, and is unlikely to be launched in 2013.

Dubai plans to source 5% of its power supply from solar energy by 2030. Last year, the Dubai Water and Electricity Authority launched the Sheikh Mohammed bin Rashid Al-Maktoum Solar Park. The project is expected to reach a capacity of 1,000 megawatts by 2030 using a combination of solar thermal power and photovoltaics. The first phase, a 13-megawatt photovoltaic plant, was awarded last year and is currently under construction.

The procurement of the first phase of the Sheikh Mohammed bin Rashid Al-Maktoum Solar Park was undertaken on a publicly-financed engineering, procurement and construction basis. Surprisingly, the Emirate of Dubai does not yet have an independent power project procurement model. Last year, the Dubai Water and Electricity Authority tendered what was meant to be its first independent power project at Hassyan; however, the project was shelved just before the preferred bidder was due to be named. The Hassyan project is soon to be reincarnated, on an independent power project basis, in the form of a two-phased 1,200-megawatt clean coal project.

The Dubai Water and Electricity Authority recently divulged details on the procurement of the second phase of the Sheikh Mohammed bin Rashid Al-Maktoum Solar Park. The project will be procured on an independent power project model. Like the first phase, it will be a solar photovoltaic project. The size of the project remains uncertain, but it seems likely that it will be a large project between 100 and 200 megawatts. Regrettably, no details have been provided on the timing for tender issuance.

Separately, Dubai is also planning to launch a solar photovoltaic rooftop program. It appears to be in more advanced stages than Abu Dhabi, reports having suggested that it is finalizing legislation for the program that would include a feed-in tariff. The program launch date is uncertain, however. At the beginning of the year, market rumors went so far as to suggest that the program had been shelved. In any event, Dubai’s solar rooftop program is unlikely to be launched in 2013.

Kuwait

Kuwait is one of the newest players in the Middle Eastern renewable energy sector. The country plans to generate 15% of its electricity from sustainable sources by 2030. The key focus is on solar power and wind.

In June this year, the Kuwait Institute for Scientific Research, or KISR, announced that it had invited pre-qualified contractors to submit bids for three pilot renewable energy projects. This is the first phase of a 2,000-megawatt renewable energy project known as the Shagaya renewable energy park that, as a whole, is due for completion in 2030.

The first phase of the park, which is scheduled for completion in the second half of 2016, is being procured on an engineering, procurement and construction basis. The overall capacity of this initial phase is 70 megawatts, comprising a 10-megawatt wind farm, a 10-megawatt solar photovoltaic plant and a 50-megawatt solar thermal plant. The strong emphasis on solar thermal mirrors the approach of neighboring Saudi Arabia.

Thirty-seven companies out of 107 pre-qualified to bid for the first phase projects, including 16 for the wind farm, 13 for the solar photovoltaic plant and eight for the solar thermal plant. The bid submission deadline is October 13, 2013.

The second and third phase projects will be procured on a build-own-and-transfer basis, with a 25-year power purchase agreement. KISR plans to procure 930 megawatts of solar power facilities in phase two and another 1,000 megawatts in phase three. It is not clear whether further wind power capacity will be procured in the second and third phases.

The renewable energy park will be built on a 39-square-mile area in Shagaya, a desert zone 62 miles west of Kuwait City and near the country’s borders with Iraq and Saudi Arabia.

In terms of power project procurement, KISR is a new player. It is therefore likely to take some time before tenders are issued for the second and third phases of the Shagaya park.

In parallel, the State of Kuwait’s Partnerships Technical Bureau is set to tender the Al Abdaliya integrated solar combined-cycle project, a 280-megawatt power project with a 60-megawatt solar power component. The solar power technology has not been confirmed. No time indication for tender issuance has been provided.

Kuwait’s Partnerships Technical Bureau is responsible for the implementation of the country’s public-private partnership program. The Partnerships Technical Bureau does not have quite as developed a power procurement model as, say, Saudi Arabia’s Saudi Electricity Company; however, it is very close to closing the country’s first independent water and power project, the 1,500-megawatt Az-Zour North project. Once that project closes, and the newly-developed Kuwaiti power procurement model emerges, then the likelihood of progress on the Al Abdaliya integrated solar combined-cycle project will be enhanced.

Qatar

Qatar plans to meet 20% of its electricity demand from renewable sources by 2030. The key emphasis is on solar power.

The only large scale solar facilities in Qatar are a 776-kilowatt solar photovoltaic rooftop system on the Qatar National Convention Center and an 800-kilowatt solar photovoltaic rooftop system on the student halls of the Qatar Foundation.

In 2012, Qatar announced plans to launch 1,800 megawatts of solar projects by 2014. A first phase of 200 megawatts was due to be tendered in the first quarter of 2013. Lack of progress has created uncertainty, however, and has led to some loss of confidence in the market.

Notwithstanding recent public spats, Qatar should be the host of the 2022 World Cup, which potentially creates a major opportunity for renewable energy players. The country has said publicly that the event would be the first carbon-neutral World Cup and explicitly said that this would be accomplished by using solar power and other renewable energy sources to power and cool stadiums.